Recognizing Early-Stage Financial Stress Before It Becomes a Collections Problem

By Heather Siebken – Director, Councils and Marketing

For many utilities, bad debt and collections are no longer a cyclical challenge; they are a structural one.

Even as processes, tools, and outreach strategies improve, the underlying issue persists; customers are often entering formal delinquency too late for early intervention to make a meaningful difference. By the time accounts reach collections workflows, the opportunity to stabilize outcomes, financially and operationally, is already narrowed.

But the more pressing issue is not just delinquency itself. It’s the transition into it.

Most utilities are relatively effective at managing accounts once they are in arrears. The harder question is why previously stable, on-time customers begin to quietly shift into financial stress patterns in the first place, and how early those signals are being recognized, if at all.

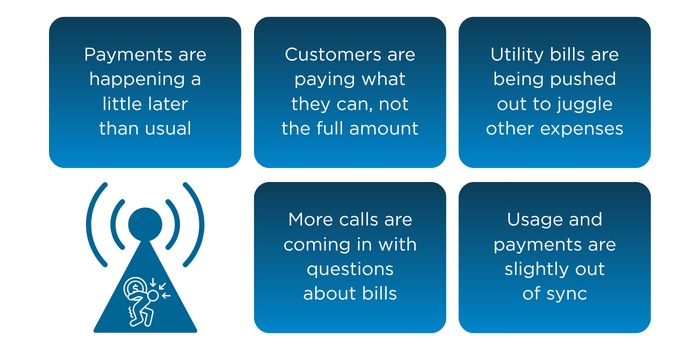

In practice, early-stage financial stress rarely appears as a single event. It shows up as a pattern: small changes in payment timing, increased partial payments, the deferral of utility bill payments to manage competing financial obligations, rising call frequency about billing clarity, or subtle shifts in usage-to-payment alignment. Individually, none of these signals are definitive. Together, they often indicate a customer beginning to lose financial stability.

The challenge is that most utility systems and operating models are still optimized to respond once thresholds are crossed, not when patterns are emerging.

This is where the opportunity is beginning to shift.

Across the industry, there is growing interest in how utilities can use existing billing, payment, and engagement data more effectively to identify early-stage financial stress without requiring major system replacements or complex overhauls. The focus is moving toward making better use of what already exists, rather than building entirely new layers of analysis.

At the same time, advances in predictive analytics, behavioral science, and AI are starting to make it possible to detect subtle changes in customer behavior earlier in the lifecycle. Not to replace human decision-making, but to surface signals that would otherwise be difficult to see at scale.

The implication is not simply operational efficiency. It is timing.

Because when utilities can identify financial stress earlier, they create more room for options that are less disruptive for both customers and the organization. That can mean more effective payment arrangements, customer programs, more targeted outreach, and fewer accounts escalating into collections cycles in the first place.

Importantly, this is not about expanding intervention for its own sake. It is about shifting engagement earlier, when outcomes are more flexible and less costly to manage.

The question is whether utilities can recognize the conditions that lead to collections soon enough to change the trajectory.

That is where the next evolution in affordability and customer financial health is beginning to emerge.

If you are interested in exploring this topic further, we are hosting a webinar on how utilities can recognize early-stage financial stress and what can realistically be done with that insight before accounts reach the point of no return. Join us to continue the conversation.

Chartwell’s ‘Put It Into Practice’ Brief

If you’re looking to move upstream of collections, the opportunity is to identify and act on early-stage financial stress before accounts escalate.

Specifically:

- Define early-stage stress signals: align on key indicators such as payment timing shifts, partial payments, and increased billing-related contact

- Use existing data more effectively: integrate billing, payment, and engagement data to identify emerging risk patterns without waiting for delinquency triggers

- Shift from thresholds to patterns: move beyond static triggers and focus on combinations of behaviors that signal declining financial stability

- Enable earlier, targeted engagement: deploy proactive outreach, payment options, and assistance programs before accounts enter collections workflows

- Measure impact upstream: track reduction in new delinquencies, improved payment consistency, and decreased flow into collections

Early identification is not about adding complexity. It’s about improving timing so utilities can intervene sooner, stabilize outcomes, and reduce the need for more costly downstream actions.

***

Heather Siebken is a product and marketing leader and customer experience expert with more than 25 years of experience driving innovation, customer engagement, and strategic growth. She currently leads councils and marketing at Chartwell, where she designs industry forums and content that help utilities establish a customer experience strategy to navigate customer expectations and digital transformation.

Heather Siebken is a product and marketing leader and customer experience expert with more than 25 years of experience driving innovation, customer engagement, and strategic growth. She currently leads councils and marketing at Chartwell, where she designs industry forums and content that help utilities establish a customer experience strategy to navigate customer expectations and digital transformation.

Previously, Heather led product development and marketing at Omaha Public Power District, where she oversaw a broad portfolio of customer energy solutions spanning energy efficiency, demand response, electrification, and customer assistance programs. She is known for her strategic foresight, storytelling, and ability to translate complex trends into actionable business outcomes.